In today’s ‘VUCA’ world—characterised by volatility, uncertainty, complexity and ambiguity— it is becoming harder and harder to get right. As discontinuity becomes the norm and the most established business models come under threat, business leaders may need to adapt their models or develop new ones.

Globalisation, technological development and rapid population growth are causing fundamental change to the business world. Traditional financial reporting has not kept pace with the seismic shift in macro-economic value experienced over the last 30 years, and this is reflected in balance sheets.

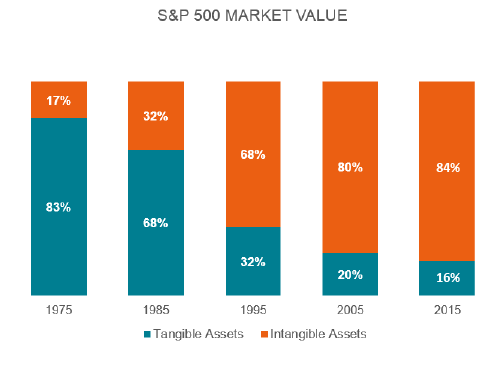

A study by the consulting firm Ocean Tomo concludes that intangible assets now make up more than 80% of S&P 500 market value, up from less than 20% in 1975. Another research from McKinsey finds 31% of Western companies’ profit comes from these “asset-light, idea-intensive sectors”, compared with 17% in 1999.

The following chart highlights the changing roles of tangible and intangible assets in terms of market value over time.

Reporting must evolve to address the information needs of business decision-makers within this changing business dynamic. The focus has to be on disclosing not just a broader set of information but the relevant and interconnected information needed by investors, employees and other stakeholders. As a result, management accounting is essential to achieve sustainable success in a constantly changing environment.

Additionally, the large majority of senior business leaders find themselves battling against bureaucratic decision-making processes, siloed and short-term thinking, breakdowns in trust and collaboration inside the organisation and difficulties with translating ever-expanding volumes of information into relevant knowledge.

Security is a major concern in our industry. Using Infor solutions was instrumental in ensuring we were delivering features with a high level of security and data privacy.

Howard Phung Fraser Hospitality Australia

TRG provides us with high-level support and industry knowledge and experience. There are challenges and roadblocks but it's certainly a collaboration and partnership that will see us be successful at the end.

Archie Natividad Aman Resorts

IT, Talent and F&B - we think it's a great combination.

We've thrived since 1994 resulting in lots of experience to share, we are beyond a companion, to more than 1,000 clients in 80+ countries.

© 2023 TRG International. Privacy Policy / Тerms & Conditions / Site map / Contact Us

TRG encourages websites and blogs to link to its web pages. Articles may be republished without alteration with the attribution statement "This article was first published by TRG International (www.trginternational.com)" and a clickable link back to the website.

We are changing support for TLS 1.0 and older browsers. Please check our list of supported browsers.

English

English  Vietnamese

Vietnamese